The rising popularity of Revenue-Based Financing among startups

Revenue-based financing (RBF) is a type of financing that is becoming increasingly popular among tech companies, particularly in the SaaS sector. Unlike traditional loans that require fixed interest payments, RBF is repaid as a percentage of future sales. This flexible repayment structure makes it an appealing option for rapidly growing businesses with high potential for future revenue.

Over the past year, the interest in RBF has surged within the tech community. To help you understand this financing option, we've compiled a comprehensive guide covering what RBF is, how it works, and when it might be the right choice for your business. Unlike traditional loans, which are paid back with interest, RBF is repaid based on a percentage of future sales. This can be a great option for businesses that are growing quickly and have a high potential for future revenue.

Over the past year, there have been an increase level of interest in revenue based finance in the tech scene. We have therefore compiled a guide on what it is, how it works and when you need to know about it for your business.

Whether you’re a SaaS company, mobile app, or tech-enabled business with recurring revenue, RBF can be a useful tool to finance growth. But it’s not without its tradeoffs. As part of a broader non-dilutive funding strategy, it offers an alternative to venture capital, especially when used thoughtfully alongside other financing methods like traditional debt.

What is Revenue-Based Financing?

Revenue-Based Financing is a funding model in which debt providers provide upfront capital in exchange for a percentage of future revenues (ARR). This continues until a predefined repayment cap is met—often 1.2x to 1.5x the original amount. It’s technically a form of debt, but unlike a bank loan, repayments are variable. If your revenue grows quickly, you repay faster. If growth stalls, repayment slows too.

At its core, RBF offers predictability on total repayment while allowing for flexibility in the timeline. That said, it’s still debt, and it can become expensive capital if used in the wrong context.

One of the advantages of RBF is that it can provide capital without putting the business owner at risk of personal bankruptcy. This can be a lifesaver for businesses that are struggling to get approved for a traditional loan. In addition, RBF can be easier to obtain than equity financing, making it a good option for businesses that are not yet ready to give up control.

However, it is important to remember that RBF is still a debt, and it should only be used if the business has a strong chance of success. If used wisely, RBF can be a great way to finance small business growth. As a startup, one of the most important things you can do is to grow your revenue. Without revenue, your startup will not be sustainable in the long term. One way to finance your startup growth is through revenue based finance (RBF).

How revenue based financing works

Revenue based financing works by providing capital to a business in exchange for a percentage of future recurring revenue & sales. The percentage of sales that is paid back to the lender can be flexible, but is typically between 1-5%. This means that if a business has $1 million in sales, they would owe the lender $10,000-$50,000. The repayment schedule is also flexible and can be weekly, monthly, or yearly.

This model avoids fixed interest and rigid schedules—but it introduces variability into your monthly cash flow. If your margins are tight, that fluctuation can cause friction.

Type of companies that are eligible for revenue based finance

There are a few key things to remember when considering a revenue based finance arrangement. First, it is important to remember that this is still a debt, and should only be used if the business has a strong chance of success. Second, the repayment schedule can be flexible, but will typically be tied to the company's sales. This means that if sales slump, the business may have difficulty making their payments. Finally, it is important to compare the terms of different financing options before deciding which one is right for your business.

Revenue based finance can be a great option for businesses that are growing quickly and have a high potential for future revenue. However, it is important to remember that this is still a debt, and should only be used if the business has a strong chance of success. If used wisely, RBF can be a great way to finance small business growth. When used correctly revenue based financing can have many benefits for startups. The main thing to remember is that it should only be used if the startup has a good chance of success and high potential future revenue.

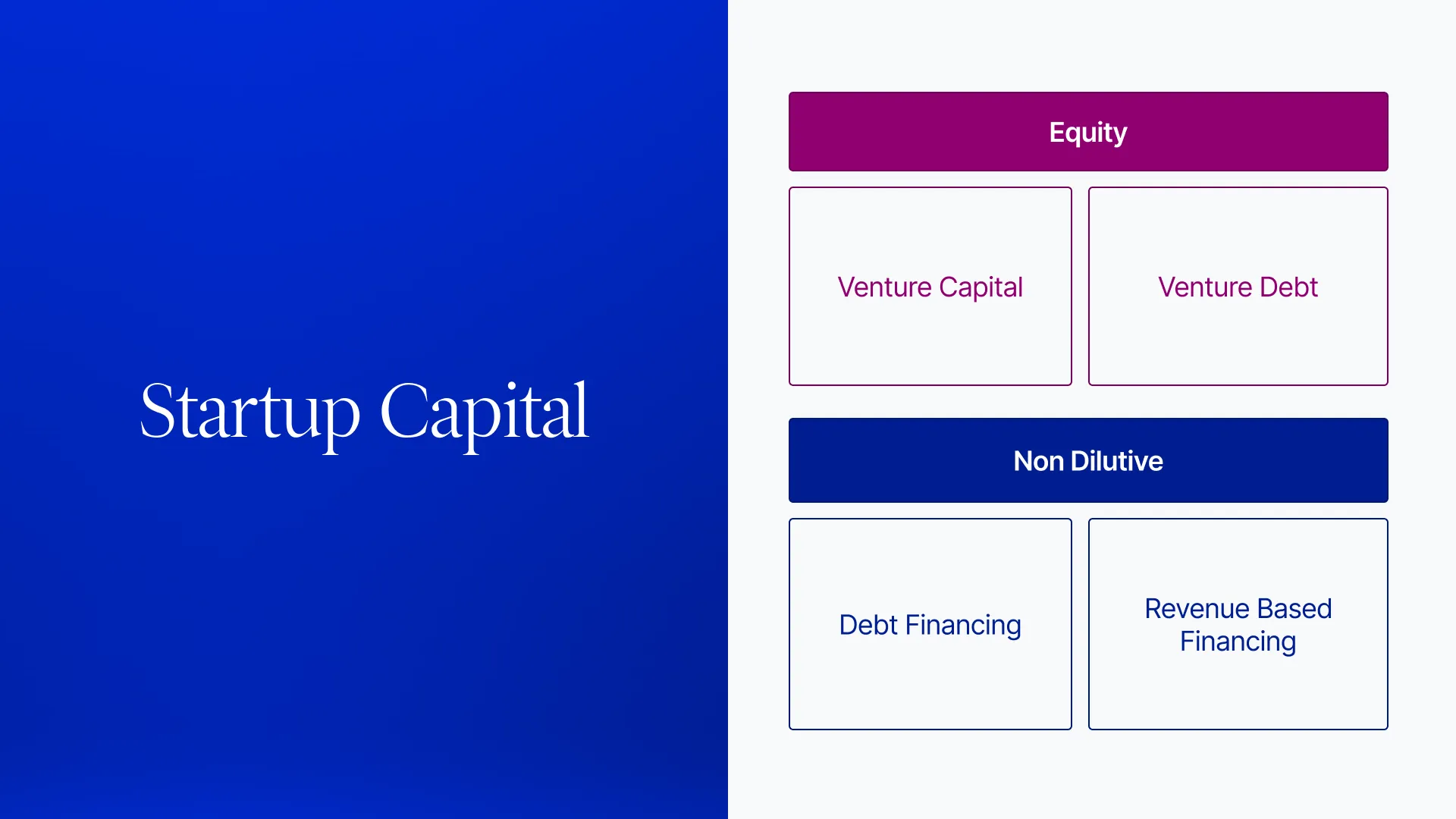

The difference of RBF and other sources of startup capital

Revenue based financing is often an attractive option for startups that do not qualify for traditional bank or venture capital funding. It provides a way to raise significant amounts of money without giving up equity in the business, and it can be structured so that payments are based on actual revenue generation rather than projections.

However, there are other types of alternative financing options for startups as well. For instance, some businesses may opt for merchant cash advances, which allow them to borrow against future sales on flexible terms. Many startups also consider venture debt och debt financing with longer repayment terms than she short time-spans for revenue based financing.

Revenue based financing can be a great way for startups to access quick capital without giving up equity. It allows businesses to borrow against future revenue with relatively low interest rates and flexible repayment terms. However, it's important for investors to understand the potential risks associated with this type of investment and compare it to other alternatives before making any decisions. With careful consideration and due diligence, revenue-based financing can be an attractive funding solution for many types of businesses.

Advantages of RBF: But Not Without Limits

RBF is often promoted as founder-friendly, and in many cases, it is. But it’s important to consider the full picture.

The Upside of RBF:

Non-dilutive: You maintain control of your company.

Aligned incentives: Funders succeed when your revenue grows.

Fast access: Compared to VC, the process is often faster and less complex.

No personal guarantees: Unlike bank loans, RBF usually doesn’t require collateral.

The Considerations with RBF:

Can be costly: Repayment caps may translate into a high effective interest rate.

Cash flow variability: Monthly repayment amounts can spike alongside revenue, creating planning challenges.

Not suitable for all models: Businesses with seasonal or inconsistent revenue may find the repayment structure unpredictable.

💬 Important: RBF isn’t a “set it and forget it” option—it requires active financial planning to avoid pressure on working capital.

RBF vs. Traditional Debt Financing

Though both are forms of debt, traditional loans and RBF serve different company profiles.

Debt Financing (Like Growth Loans):

Banks or specialized lenders provide capital with:

Fixed repayment schedules

Interest-bearing terms

Clear end dates and maturity terms

Best for: Startups with more stable, predictable cash flow and asset-backed models.

Revenue-Based Financing:

Repayment percentage tied to monthly revenue

No compounding interest

Total repayment amount capped but variable timeline

Best for: SaaS or subscription businesses with recurring revenue and growth opportunities.

Combining both methods—sometimes called a "capital stack"—can balance cost and flexibility.

Potential risks associated with Revenue based financing

Revenue-Based Financing has its place in a modern startup capital strategy. It’s flexible and non-dilutive, but it’s still debt—and should be treated as such. With proper forecasting, strong revenue visibility, and a clear use of funds, it can be a powerful tool to fund the next phase of your growth.

If you're considering RBF, approach it with the same scrutiny you would any funding source. Match the tool to the task.

One key risk to consider when investing in revenue-based financing is that the return on investment depends on the business being able to generate enough revenue to pay back the loan. If the business does not perform as expected or fails altogether, then investors may not receive their expected returns. Additionally, if the company cannot make timely payments, it could face reputational damage from creditors who will view its failure to repay as an indication of poor management and fiscal irresponsibility.

Revenue-based financing is also subject to market risk, as the value of investments may fluctuate with changes in the broader economy and financial markets. This can create additional volatility for investors who are looking to diversify their portfolios with alternative forms of lending. Additionally, revenue-based financing investments may not be liquid asset investments, meaning that it may take time to sell or convert an investment into cash if needed.

In terms of payback time of your loan, revenue based finance actors usually need to have repayment of 0,5-2 years which also sets a lot of pressure to pay back in a short period of time of the company taking the financing through this option.